Last Updated on 10 February, 2024 by Trading System

ADX is one of the most popular trading indicators and is used by traders all over the world to find profitable entries and setups!

The best timeframe and settings for ADX vary by market, timeframe, and strategy. However, by using backtesting, which we do in this article, you’ll be able to at least find the settings that have worked best historically for a strategy.

In this article, we’ll explore the best settings for the ADX indicator. We’ll have a look at the performance of two setups, to see which ADX settings that seem to work the best.

Let’s start!

Important!

The tests in this article will be carried out on the SPY ETF, which tracks the S&P-500. Markets differ a lot, and you should always check to see so that your strategies and ideas work as you expect them to, before going live. This is explored in more depth in our article on how to build a trading strategy.

You should also be aware that historical results are not indicative of future results. This means that the results presented may only be the result of random chance, and may not hold any value going forward. This is covered in greater detail in our article on curve fitting!

Which Settings Are Best for ADX?

The most common settings for ADX usually are a 14-period length together with a high volatility threshold at 25, and a low volatility threshold at 20. In other words, a market is thought to be volatile when ADX is above 25, and calm when it’s below 20.

Now, to answer the question we first need to know whether our strategy benefits from high or low volatility. Since there are as many strategies as there are traders, it would be an impossible task to give some form of general advice. Due to that reason, we’ll focus on one of the most common ADX trading strategies, which is the DMI-plus and DMI-minus Crossover strategy.

We’ll also cover a breakout logic, where we’ll buy on a 10-day high. There we’ll see whether a high or low ADX reading works best, and what settings that seem to have produced the best results historically!

Testing the Best Settings for DMI Crossovers

We’ll start off by just testing the default DMI crossover strategy. We’ll buy when the 14-period DMI-plus crosses above the 14-period DMI-minus, and sell once the former crosses below the latter.

Here are the results:

As you see, the strategy seems to work well in bull markets. Still, this isn’t something we’d like to trade in its raw form!

So how could we go about improving the strategy?

We’ll one common approach is to demand that ADX is above 25. However, in our tests, we’ve found out that a low ADX reading actually works better, so let’s try that!

We require that DMI-plus is above DMI-minus and that the 14-period ADX is below 20, to enter a trade.

The results are visible below:

As you see, the results get a little better with the ADX-filter, but we still have quite some drawdown. The number of trades is much smaller as well.

Optimizing the ADX Settings

Let’s now have a look at how te the strategy fares when we use the same strategies as above, but look for better ADX settings!

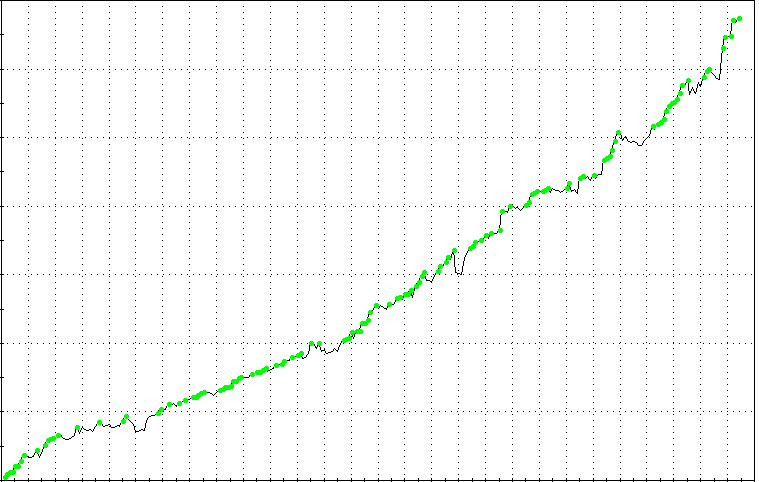

First off, we have the simple DMI-strategy without the ADX filter. When optimizing the values, we found that the best settings were 12 for DMI-plus, and 10 for DMI-minus. The following curve was what we got with those parameters:

As you see, the strategy seems to work much better with these settings!

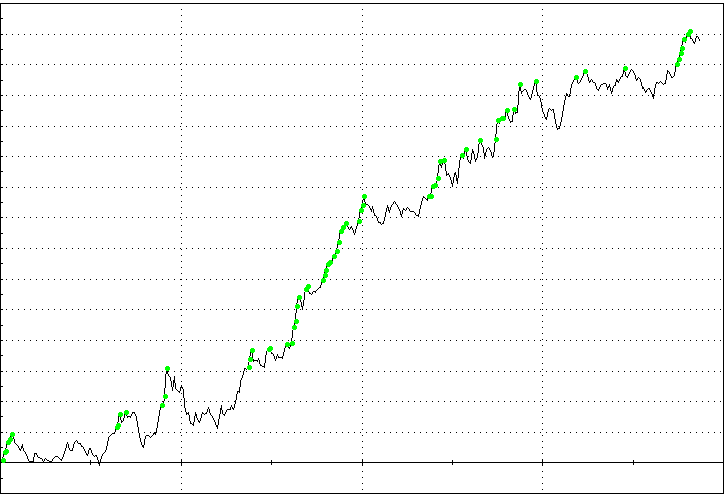

Let’s now impose the ADX filter as well!

After trying some different values, we found that the strategy worked best when the 14-period ADX was below 25, which yielded the following curve:

Conclusion

Historically, it seems like the best settings for the ADX DMI-crossover system have been:

- 12 for DMIplus

- 9 for DMI-minus

- 14 for ADX, and only taking trades when ADX is below 25.

Again, if you don’t know what curve fitting is, we highly recommend that you read our article on how to build a trading strategy. You’ll understand why we stress this so much once you’ve fully understood what curve fitting is, and how it impacts strategy testing!

Let’s now head over to the next trading strategy on our list!

Testing the Best Settings for a Breakout Logic With ADX

Let’s now test ADX with a breakout system. We’ll buy on the 20-day high, and sell 10 bars later. Here are the results for these, without any ADX-filter:

Not that promising right?

So let’s see if we can be helped by the ADX!

By requiring that the 3-period ADX is below 50 we achieved the best equity curve, with the following result.

Summary

For this strategy, it seemed like the best ADX settings were 3 for the length, and 50 for the threshold value.

What Settings Should You Use Then?

We’ll be clear!

There are no “best” settings, even if some trading educators may want you to think so!

What works best will vary depending on the market and timeframe you trade, as well as the trading strategy that’s used.

For instance, we have strategies that work extremely well with the 5-period ADX, while others only work with the 20, or even 30-period ADX!

This is why it’s paramount that you learn how to test your ideas BEFORE you go live. Many times the trading ideas you believe are going to work prove useless, and may lead to instant losses if traded with real money!

You might be interested in this article also: ADX Trading Strategy – The Perfect “Number Two” Indicator

The best way to avoid this is to learn backtesting with Easylangauge. In our extensive guide to backtesting, this is covered in more depth!

Conclusion

In this article, we’ve had a quick look at some common trading strategies in which ADX has been used either to improve a strategy or as a main part of the strategy logic.

What we’ve found is that the best ADX settings vary greatly with the market, timeframe, and strategy that’s traded. This in turns calls for the need of backtesting or other validation methods.

Still, no method is bulletproof, and when using backtesting, we always face the risk of curve fitting!

FAQ

What Are the Best Timeframe and Settings for the ADX Indicator?

The optimal timeframe and settings for the ADX indicator depend on the market, timeframe, and trading strategy. Backtesting is a useful method to determine historical performance and identify settings that have worked best for a specific strategy.

What is the DMI Crossover Strategy, and How Can ADX Improve It?

The Directional Movement Index (DMI) crossover strategy involves buying when the DMI-plus crosses above the DMI-minus and selling when the opposite occurs. Adding an ADX filter, such as requiring a low ADX reading, can help improve the performance of the strategy.

How Can ADX be Applied to a Breakout Logic Trading System?

Applying ADX to a breakout logic system involves buying on a high and selling after a certain period. In this case, requiring a low ADX reading, like 3 for the length and 50 for the threshold, has shown to improve the equity curve for breakout strategies.