Last Updated on 10 February, 2024 by Trading System

Average True Range

Average True Range (ATR) is a technical tool that is used to measure volatility. Volatility is important because it is a reliable proxy for risk in the market. Since all investors aim to maximize risk-adjusted-returns, it makes sense to have a measure of risk as part of one’s decision matrix. An investor that knows how to read ATR will be able to use it with different strategies. The two most common strategies for ATR are judging the speed of movement and adjusting the stop loss mechanism to changing volatility.

What is ATR?

Average True Range (ATR) belongs to a group of technical tools that are used to measure volatility. This in-turn, allows the investor to integrate risk into their decision making. ATR is used in different types of markets. Though ATR is a strong measure on its own, it can also be used in conjunction with other measures. All measures for price can be judged on their ability to measure the direction or strength of price movements. ATR cannot be used to measure the direction of the price movement. Therefore, it is often prudent to use it along with a trend indicator.

Now there are some important points that every investor must know about ATR before they can use it to maximize their risk-adjusted-returns. First, ATR can measure volatility over any time period. There is a convention to use 14 days. However, the optimum time for ATR depends on the market that is being studied and the strategies being used by the investor. Second, ATR can be used for any time frame be it day, months or weeks. This again depends on the dynamics of the market. At this point one must realize that a tool is only as good as the market domain knowledge of the investor. Before one knows how to use ATR, it is important to understand how ATR is calculated and the importance of volatility for investors. Let’s start with the importance of volatility for investors.

Where Is Volatility Important?

Volatility is relevant to the investor because of the concept of risk. Every investor has to choose between different investment options. All of these options promise returns. At first look, it makes natural sense to choose the investment with the highest returns. However, prudent investors realize that these returns are not guaranteed. For two promising investments, one investment might fulfill its promise while the other one might even give negative returns. Though these investments are not guaranteed, some investments are more sure bets than others. These sure bets are said to carry a lower risk as compared to their more uncertain counterparts. Therefore, it’s no surprise that good investors also consider the risks along with the returns and always perform their comparative analysis on the basis of risk-adjusted-returns.

In order to calculate the risk adjusted returns, the investor needs to take a proxy (something that represents risk) for risk. Volatility is a good proxy for risk. Volatility measures help investors with the comparing risky investments (with high returns) to low risk investments (with comparatively lower returns). ATR is one of those measures of volatility. In order to fully grasp the use of ATR, one must understand the formulae used to calculate ATR.

How do you calculate ATR?

ATR is essentially a moving average of the true range. True range is calculated for every time period. The first true range is simply the high minus low. For the following true range values, the formulas are as following:

True range = MAX (BarHigh, PreviousBarClose) – MIN (BarLow, PreviousBarClose)

Alternatively, it can also express as following

True range = Whichever-is-higher(BarHigh, PreviousBarClose) – Whichever-is-lower(BarLow, PreviousBarClose).

The above statement contains three different formulas depending on if there was a price gap or not. A price gap occurs when the price ticker between two consecutive time periods has a gap. The red circles in the following image show an example of such price gap.

Source: https://forexsignal30.com/what-is-a-price-gap-in-forex-trading/

The price gap can be of two types. First, the current opening can be lower than last close, which is what is happening for the above price chart. Otherwise, the previous close can be lower than the current opening. This is what happens in the image below.

Source: https://www.investopedia.com/terms/g/gap.asp

For each of these situations, the calculation for true range is given as follows

- No gap: current-high – current-low

- Positive gap: absolute value of |Current-high – previous-close|

- Negative gap: absolute value of |Current-low – previous-close|

Once one has the TR values for all the days, then ATR can be calculated via a moving average.

If the investor is finding the ATR for n time-periods then the ATR for the first day is the Average of True range for the last (n-1) days. While the ATR for the n+1th day is given by the following formulae

This formula is used to get a series of ATR values. Of course in real life investors prefer ATR graph as compared to tables of ATR values.

How To Use ATR?

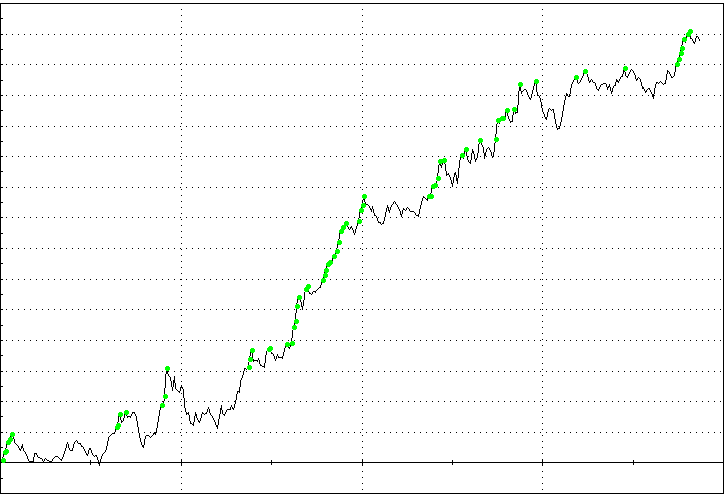

An investor cannot use ATR unless they know how to read graph for ATR. The following image shows the graph that the investor uses while trading with ATR.

Source: https://www.youtube.com/watch?v=4gUM11OzFpo

The circled red line above shows the value of the ATR. As the ATR increases so do the volatility. These changes in ATR can be used by the investor to adapt to the changing volatility within markets. Below are some of the strategies used by investor to maximize their risk adjusted returns

Using Average True Range (ATR) In Trading

Finding the pressure of the move

If there is a reversal in the direction, that reversal can be steep or slow. An investor needs to know the speed of this reversal in order to calculate their expected-annualized-gains from investment. Usually, the rule of thumb is that the higher the change in ATR, the more explosive the move. This definition of explosiveness varies depending on the market. What is considered explosive for S&P 500 might be just another day for Penny Stocks. Remember it is the change in the value of ATR that betrays the pressure rather than the absolute value for ATR. By looking for changes in the value of ATR, one can get a fair idea of the strength of the current market move.

Use ATR to adjust top loss

All investors need to trail their investments with a stop loss order. Stop loss orders automatically sell assets if they move above or below a certain threshold[1]. These stop-loss measures can be placed on a percentage or absolute basis. in percentage basis the stock is automatically sold after it changes in value by a certain percentage whereas in absolute terms the sale happens as soon as the stock crosses a certain threshold.

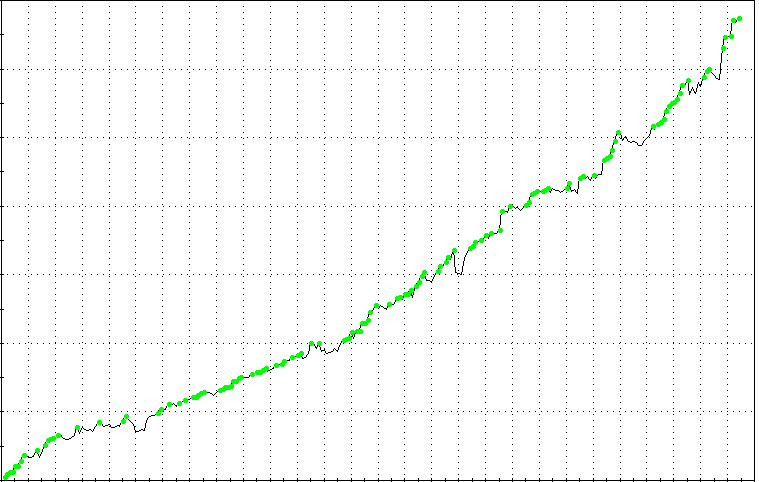

Creating a stop-loss can become a problem if the stop-loss sells an asset too soon. In the following image we can see that if the investor had placed his stop loss at the red line, they would have lost on the rally afterwards. Under fixed market volatility, these mistakes can be corrected on the basis of experience. However, with changing volatility the investor risks repeating the same mistake over and over again. ATR can help the investor in adapting to the changing volatility. If the investor keeps their stop-loss order as a multiple of ATR, they would avoid selling the security too soon. The exact multiple would again depend on the market and intuition of the investor.

What are the upsides and downsides of using ATR?

Like all measures ATR has its advantages and disadvantages. Good investors will play to the strengths of ATR while making up for its weaknesses. The defining advantage of ATR is that it is able to measure volatility even when there are price gaps. The aim of using ATR is that investor should be warned about sudden increase or decrease in volatility. Any measure that cannot measure volatility over price gaps is will fail badly at warning the investor of such changes in the volatility. Furthermore, ATR can also be used for any length of time period (1-1000) or time frame (hours, days, weeks, years). This allows investors with different types of strategies to use ATR.

On the flipside, ATR cannot measure changes in direction. This ability is not something one looks for in a volatility measure, but it is always useful. However, one must realize that no tool is meant to be used alone. Prudent investors will always use ATR with some other measure such Bollinger bands.

Conclusion

ATR is a good technical indicator that can be used to measure the volatility in a market. The measure is essentially the moving average of the true range value for the given time period. Investors can use ATR to find the pressure of the rally or run. Furthermore, ATR can also be used to adapt the stop-loss mechanism to changing volatility within the market. As long as one uses ATR along with a direction-assessing technical measure, this tool can come in very handy when it comes to maximizing risk adjusted returns.

[1] The value and direction of these thresholds are determined by whether the investor is going for a short or long position.

FAQ

What are the key points to know about ATR before using it for risk-adjusted returns?

Before using ATR, investors should be aware that it can measure volatility over any time period, with a common convention being 14 days. The optimal time frame for ATR depends on the market and the investor’s strategies. It’s crucial to understand how ATR is calculated and its significance in assessing volatility for effective risk management.

How can ATR be used in trading, and what does the ATR graph represent?

In trading, ATR can be used to gauge the volatility of the market. The ATR graph shows changes in ATR values, indicating changes in market volatility. Traders can adapt to varying volatility by observing these changes. The ATR graph is a valuable tool for implementing strategies that maximize risk-adjusted returns.

What are the advantages and disadvantages of using ATR?

ATR’s strengths lie in its ability to measure volatility, even in the presence of price gaps. It can be applied across different time periods and time frames, accommodating various trading strategies. However, ATR does not measure changes in direction, and prudent investors often use it in conjunction with other measures, such as Bollinger Bands, to complement its limitations.